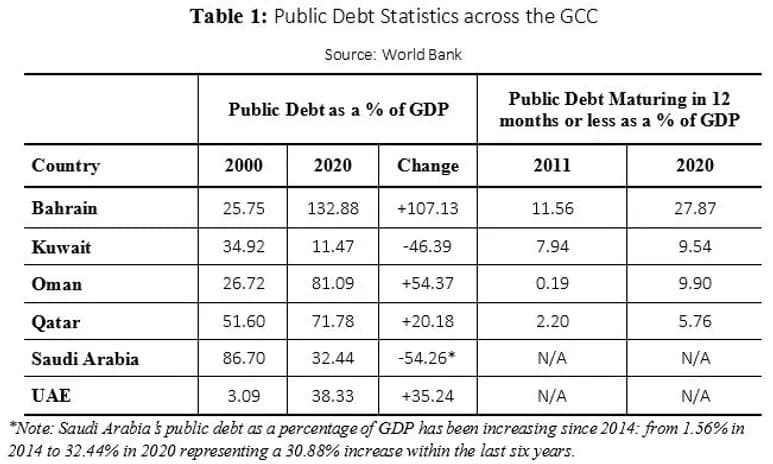

The COVID-19 pandemic has had both wide-ranging and far-reaching consequences. From disruptions to education and the straining of public healthcare systems, to the crippling of global supply chains and an ensuing economic downturn. While it is still too early to measure the full impact of the pandemic in the medium and long runs; it is safe to say that the pandemic has led to the deepest recession since the Great Depression.[i] Globally, central banks have coordinated efforts to slash interest rates to record lows in order to promote demand, and government spending has increased to offset health and economic needs. This fiscal relaxation has led to dramatic increases in public debt ratios in both advanced and emerging market economies. The Gulf Cooperation Council (GCC), faced with the double impact of both the pandemic and low oil prices, tapped into the international debt market to issue over $60 billion (USD) to meet rising financial needs, above the total issuance of $44 billion (USD) in 2019.[ii] This has led to a ballooning of publicly held debt within the GCC. However, this is not an altogether new, as debt ratios within the region have already been in steady incline for much of the past two decades. Table 1 showcases this trend via public debt ratios within the GCC in the year 2000 compared to 2020, as well as the ratio of public debt maturing in 12 months or less in both 2011 and 2020.

Public debt ratios have increased in most GCC countries, with figures ranging from 20% to over 100% of GDP over the past twenty years, and over US$100 billion in debt is maturing between 2021 and 2025 which will increase financing needs in the short term.[iii] The question is, with fiscal dependence on oil and historically volatile oil prices, is the public debt within the GCC sustainable? This paper aims to assess public debt sustainability in the GCC and discuss possible fiscal policy considerations in light of this increase in debt.

When is Public Debt Sustainable?

The question of public debt sustainability has dominated macroeconomic discourse since post-WWII reconstruction efforts led to a sharp increase in public debt across advanced economies. Theoretically, public debt is considered sustainable as long as economic growth rates remain firmly above real interest rates;[iv] which would make it feasible for economies to service mounting debt and organically reduce the debt-to-GDP ratio via economic growth. Researchers have also presented other criteria such as debt-to-GDP thresholds as a form of debt sustainability, whereby economies exceeding such thresholds would experience slower growth making it harder to service debt and organically reduce its ratio to GDP. These thresholds range from 77%[v] to 115%[vi] of GDP. Other researchers believe the ratio of external debt to GDP to be more pressing, with some suggesting thresholds between 20-25%[vii] and 35-40%[viii] as ceilings beyond which there is significant impact on economic growth prospects. Some researchers claim that public debt can only be considered sustainable when it is proven that policymakers adjust fiscal policy to changes in the primary balance.[ix] In a working paper for the International Monetary Fund, Pescatori, Sandri and Simon (2014)[x] refute the existence of debt thresholds by showing that economies with high debt-to-GDP ratios can still experience solid growth performance, and instead, stress a country’s debt trajectory as the key indicator. That is, a country with decreasing debt will experience a higher growth rate than a country with increasing debt regardless of debt level.

Debt sustainability is, thus, a complex and multifaceted issue. A host of other indicators such as the size of the fiscal multiplier, the degree of trade openness and the marginal propensity to import can change public debt dynamics within an economy. Other country-specific factors such as the accumulation of public capital, infrastructure needs and levels of private demand are equally important factors to consider when making public debt tradeoffs. Research has shown that the context in which borrowed funds are used plays an important role in understanding debt sustainability largely because certain spending either pays for itself or more than pays for itself in the long run.[xi] Even then, sustainability is difficult to measure for the simple fact that policymakers must rely on forecasts, which are inherently uncertain.

The wide consensus, then, is that under most conditions, possessing, maintaining and especially increasing public debt is undesirable. Most major advanced economies, however, continue to live with permanent deficits and increasing public debt ratios. Empirical results have shown that the rate of public debt growth in member countries of the Organisation for Economic Cooperation and Development (OECD) far exceeds economic growth rates.[xii] Public debt exceeds over 100% in both the United Kingdom and the United States, and is over 200% in Japan. Yet the narrative around public debt in advanced economies is seldom as consequential as it is for the GCC, who, despite maintaining lower, and relatively more manageable public debt ratios (see Table 1), have been the target of multiple credit rating downgrades in the past decade. Are public debt management dynamics different for the GCC, and has the sustainability of public debt within the region become compromised?

The GCC’s Rising Public Debt Stock

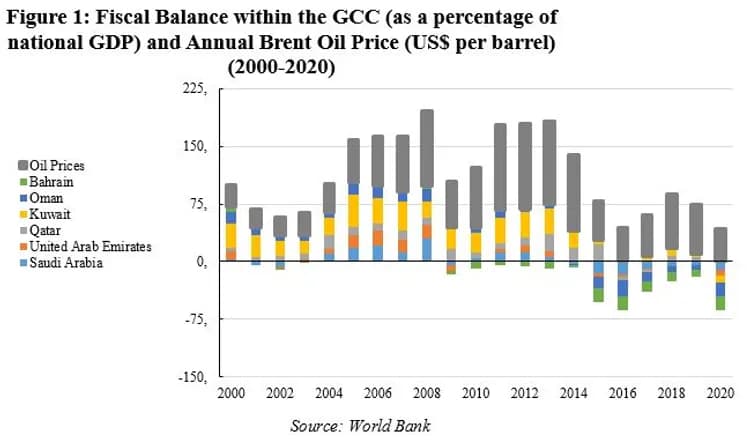

To assess public debt sustainability, one must first understand the context with which public debt stock has risen within the region. While sustainability issues vary by country, the GCC is discussed collectively in this paper because, among other aspects, they share similar economic make-up, coordinate monetary and fiscal policies, and possess synchronised business cycles.[xiii] Figure 1 below showcases fiscal balance within the GCC between the years of 2000 and 2020.

During the time of rising oil prices throughout the mid-to-late 2000s, the GCC amassed large surpluses despite announcing ambitious diversification plans. Widening fiscal deficits began, in earnest, after the financial crisis of 2007-2008. Figure 1 also shows that fiscal balance has been largely dependent on oil prices, and with each GCC country having different oil-price breakeven points, some countries were affected more so than others. Following the Oil Glut of 2015, however, the GCC experienced chronic fiscal deficits (with the exception of Kuwait) as oil prices settled on a new, lower, equilibrium. This, coupled with current account deficits, led to a sharp decline in public finances that necessitated debt issuance to cover recurring costs. Consequently, the GCC coordinated the implementation of substantial fiscal consolidation measures such as subsidy cuts, public (often current) spending cuts, and value-added-tax (VAT) to offset debt accumulation.

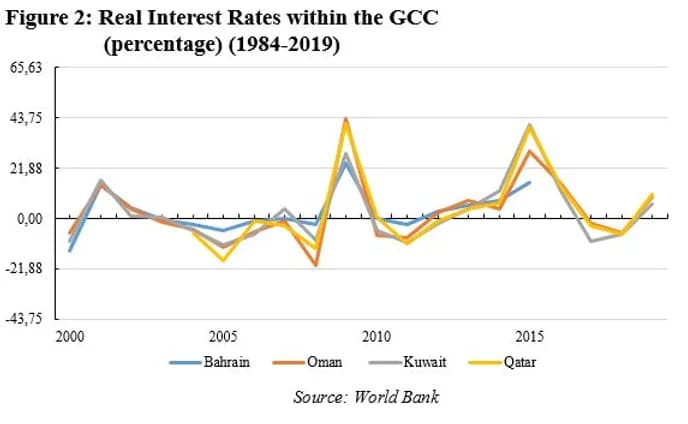

Some researchers have claimed that these measures were implemented too quickly and have not only negatively impacted growth in the short term, but also stalled diversification plans necessary for long-term sustainability.[xiv] Yet the International Monetary Fund (IMF) as well as leading sovereign credit rating agencies remain skeptical about the GCC countries’ fiscal sustainability and continue to call for more substantial and sustained consolidation measures.[xv] So why is the GCC’s fiscal position so compromised? Ultimately, it boils down to the GCC’s fiscal dependence on non-renewable natural resource rents. Oil prices have been all but reliable in the past, and with global green energy initiatives already underway, they are likely to remain volatile in the foreseeable future. Until diversification measures bear their fruit, and until the private sector becomes the primary driver of growth, then there will always be heightened fiscal sustainability risks. This, perhaps, is why, as displayed in Figure 2, real interest rates within the region have generally been volatile. Unlike major developed economies, the GCC contends with relatively higher interest rates on average that make their bonds both inherently riskier and more expensive. International demand for GCC bonds have not weakened, however, despite aforementioned skepticism.[xvi]

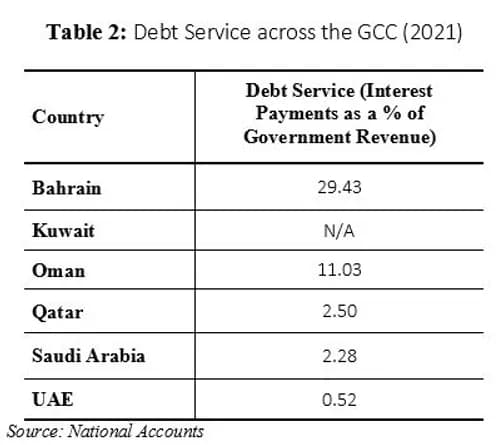

This shows that, while fiscal dependence on oil weighs down on GCC public debt sustainability, it is not the only thing international investors and creditors consider. The GCC’s low debt exposure (especially when compared to other high income economies), sizeable sovereign wealth funds, reliable foreign reserves and — as showcased by Table 2 below — relatively low debt service ratios (with notable exceptions in Bahrain and Oman) have helped retain international business confidence and allowed for a steady flow of capital to the region.

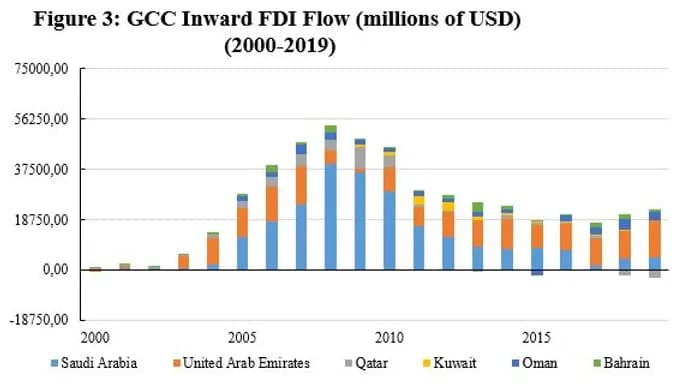

The GCC continues to attract significant foreign direct investments (see Figure 3 below), even when global trends would suggest otherwise. While investment flows have peaked within the region right before the financial crisis, the GCC continues to attract investments worth billions of US dollars each year. For instance, despite a global decline of 42% in FDI in 2020, heavily indebted Bahrain was still able to attract over US$1 billion in foreign investments last year, marking a 3.3% increase in total FDI stock.[xvii]

Despite the accumulation of debt, even the most indebted nations of the GCC, continue to post impressive growth figures, remain attractive investment destinations and still retain considerable debt market access. There is also significant room for potential growth, especially in light of diversification measures, and most GCC countries possess the necessary fiscal buffers to contend with increasing fiscal pressure. Therefore, in terms of fiscal solvency and market access, researchers agree that the GCC’s public debt is sustainable at least in the short term,[xviii] despite certain reservations. But while there may be fiscal room today, the building up of public debt and the depletion of fiscal buffers (which the IMF forecasts by 2034 barring reform)[xix] is a serious threat to sustainability within the GCC in the medium term.

Fiscal Policy Considerations

There are two primary fiscal policy considerations for the GCC. First, it is important to deal with — particularly explosive — debt accumulation so as to retain debt market access, and to maintain the fiscal buffers necessary for a “rainy day.” If recent history has proven anything, it is that, especially with increased globalisation, there is a particularly increased risk of experiencing negative transient shocks and governments will need to absorb them — especially with declining influence of monetary policy. An added fiscal pressure for the GCC is their need to manage external debt in particular to defend against speculative attacks on their currency peg to the US dollar.[xx] This is particularly important because the surge in public debt within the region is largely attributable to a surge in external debt.[xxi] There must always be a conscious effort by GCC states to manage their debt levels;[xxii] and fiscal policy must respond to debt accumulation even if states have low levels of debt, and even if future plans necessitate further financing. This added layer, while in theory also true for advanced economies, is primarily important for the GCC because of added geopolitical risks.

The second policy consideration is that this need for fiscal adjustment must not come at the cost of growth and diversification measures. Researchers agree that, especially during volatile economic conditions, the need for stability overweighs the need to sustain debt because the risk of prolonging an already disastrous recession is far greater than the risk of defaulting. Once the pandemic has passed, however, lower real interest rates, and a pressing need for public capital stock within the region to carry out diversification plans presents a tradeoff for GCC states, whereby debt accumulation can create the impetus for greater economic growth which can rapidly lower the debt to GDP ratio organically.[xxiii] This will invariably lead to greater volatility in the short run, especially in already highly indebted countries, but can more than pay off for itself in the medium to long run so long as borrowed funds are used efficiently. There must be a delicate balance between managing current public debt levels vis-à-vis long term goals. Should the need be pressing enough, GCC governments can increase tax income, as they have in the latter half of the 2010s with the introduction of the VAT. Distortionary taxation should be a last resort, however, to avoid a considerable drop in either demand or FDI that would lead to lower growth.

***

While seemingly straight-forward, the question of public debt sustainability will almost always lead to convoluted and sometimes contradictory answers. In some cases, like the GCC, debt can be both sustainable in some ways and unsustainable in others. Some researchers have raised concerns about the accumulation of publicly held debt in both major advanced and emerging market economies, especially during COVID-19 pandemic. Other researchers, wary of the disastrous effects of early austerity measures implemented after the financial crisis, and supported by lower interest rates, believe debt to be a less pressing issue for now.[xxiv] But the need to build fiscal buffers capable of absorbing future shocks is more pressing today than ever before, and lower interest rates need not mean low forever. In the short to medium term, however, while diversification plans are still underway, the GCC must find a balancing act of keeping enough of a buffer to absorb negative shocks should the need arise, while also providing the public capital stock necessary to boost non-oil growth and accelerate the pace of diversification measures.

Resources

- International Monetary Fund. (2020). (Report). Economic Prospects and Policy Challenges for the GCC Countries. Retrieved August 2021, fromhttps://www.imf.org/en/Publications/Policy-Papers/Issues/2020/12/08/Economic-Prospects-and-Policy-Challenges-for-the-GCC-Countries-49942

- Ibid., p. 15.

- Ibid.

- Hamilton, J., & Flavin, M. (1986). On the Limitations of Government Borrowing: A Framework for Empirical Testing. American Economic Review, 76(4). https://doi.org/10.3386/w1632.

- See Caner, M., Grennes, T., & Koehler-Geib, F. (2010). (Working paper). Finding the Tipping Point—When Sovereign Debt Turns Bad. The World Bank, Policy Research Working Paper Series, 5391. https://openknowledge.worldbank.org/bitstream/handle/10986/3875/WPS5391.pdf?sequence=1&isAllowed=y

- See Minea, A. & Parent, A. (2012). (Working paper). Is High Public Debt Always Harmful to Economic Growth? Reinhart and Rogoff and Some Complex Nonlinearities. CERDI (University of Auvergne). http://publi.cerdi.org/ed/2012/2012.18.pdf

- See Clements, B., Bhattacharya, R. & Nguyen, T. Q. (2003). (Working paper) External Debt, Public Investment, and Growth in Low-Income Countries. International Monetary Fund.https://www.imf.org/external/pubs/ft/wp/2003/wp03249.pdf

- See Pattillo, C., Poirson, H., & Ricci, L. (2002). (Working paper). External Debt and Growth. International Monetary Fund. https://www.imf.org/external/pubs/ft/wp/2002/wp0269.pdf

- Beqiraj, E., Fedeli, S., & Forte, F. (2018). Public Debt Sustainability: An Empirical Study on OECD Countries. Journal of Macroeconomics, 58, 238–248. https://doi.org/https://doi.org/10.1016/j.jmacro.2018.10.002

- Pescatori, A., Sandri, D., & Simon, J. (2014). (Working paper). Debt and Growth: Is There a Magic Threshold? International Monetary Fund. Retrieved August 2021, from https://www.imf.org/external/pubs/ft/wp/2014/wp1434.pdf

- Furman, J., & Summers, L. (2020). (Working paper). A Reconsideration of Fiscal Policy in the Era of Low Interest Rates. Brookings. Retrieved August 2021, from https://www.brookings.edu/wp-content/uploads/2020/11/furman-summers-fiscal-reconsideration-discussion-draft.pdf

- Curtasu, A. R. (2011). How to Assess Public Debt Sustainability: Empirical Evidence for the Advanced European Countries. Romanian Journal of Fiscal Policy, 2(2), 20–43. https://doi.org/https://www.econstor.eu/bitstream/10419/59806/1/717988449.pdf.

- Osman, M., Louis, R. J., & Balli, F. (2010). Which Output Gap Measure Matters for the Arab Gulf Cooperation Council Countries (AGCC): The Overall GDP Output Gap or the Non-Oil Sector Output Gap? International Research Journal of Finance and Economics, (35), 7–28. https://doi.org/https://web.viu.ca/rosmyjl/Output_Gap_Measure_irjfe_35_01.pdf

- El Mahmah, A., & Kandil, M. (2019). Fiscal Sustainability Challenges in the New Normal of Low Oil Prices: Empirical Evidence from the GCC Countries. International Journal of Development Issues, 18(1), 109–134.

- See IMF (2020), p. 4.

- Narayanan, A., & Ismail, N. (2020, May). Bahrain Sells Riskiest Eurobond Since Market Reopened. Bloomberg.com. Retrieved August 2021, from https://www.bloomberg.com/news/articles/2020-05-07/bahrain-offers-riskiest-eurobond-since-market-re-opened?sref=PhzhRqBB

- Economic Development Board of Bahrain (2021, June). Bahrain’s FDI Inflows Reach $1 Billion in 2020. Retrieved August 2021, from https://www.bahrainedb.com/latest-news/bahrains-fdi-inflows-reach-1-billion-in-2020/

- See Taher (2016); and El Mahmah & Kandil (2017).

- Mirzoev, T., Zhu, L., Yang, Y., Zhang, T., Roos, E., Pescatori, A., & Matsumoto, A. (2020). (rep.). The Future of Oil and Fiscal Sustainability in the GCC Region. International Monetary Fund. Retrieved August 2021, from https://www.imf.org/en/Publications/Departmental-Papers-Policy-Papers/Issues/2020/01/31/The-Future-of-Oil-and-Fiscal-Sustainability-in-the-GCC-Region-48934

- See El Mahmah & Kandil, p.

- Waheed, A. (2016). Sustainability of Public Debt: Empirical Analysis for Bahrain. Journal of Internet Banking and Commerce, 21(2). https://doi.org/https://www.icommercecentral.com/open-access/sustainability-of-public-debt-empirical-analysis-for-bahrain.pdf

- See Hamilton & Flavin, p. 19.

- Ostry, J., Ghosh, A., & Espinoza, R. (2015). (rep.). When Should Public Debt Be Reduced? International Monetary Fund. Retrieved from https://www.imf.org/external/pubs/ft/sdn/2015/sdn1510.pdf

- Giles, C. (2020, October). IMF Says Austerity is Not Inevitable to Ease Pandemic Impact on Public Finances. Financial Times. Retrieved August 2021, from https://www.ft.com/content/722ef9c0-36f6-4119-a00b-06d33fced78f